New RICS Guidance

Why is Japanese Knotweed considered such a problem?

Japanese Knotweed is listed on schedule 9, part 2 of The Wildlife & Countryside Act 1981, making it an offence under section 14(2)(a) of the Act to ‘plant or otherwise cause it to grow in the wild’. It is an invasive and potentially destructive plant, that in certain conditions has the capacity to cause damage to poorly constructed and very old outbuildings, drains, paths, and underground services, causing heave in tarmac or poorly laid concrete surfaces. It is widely considered as the most invasive non-native species of plant within the UK & Ireland today.

Should you have any thoughts of selling your home or another property, irrespective of how small the infestation we would strongly recommend you adopt a pro-active approach to having the infestation assessed and treated by a suitably qualified professional. Conversely, we would advise anyone who is interested in purchasing a property affected by Japanese Knotweed to proceed as normal. Providing there is a treatment plan in place by a fully qualified & reputable contractor which also has a 5 or 10 year independently written Insurance Backed Guarantee (IBG), then there really is not a great deal to be concerned about. It may actually work out to your advantage in the negotiating phase!

Be pro-active as opposed to reactive. It will undoubtedly pay dividends in the long term!

Whilst Japanese Knotweed is clearly an issue to property owners, we are very careful not to overstate or exaggerate the facts – The cases of Japanese Knotweed actually reaching a point whereby it causes substantial damage to property are thankfully, somewhat infrequent. Quite often, the root cause may well be due to other contributing factors such as poor construction, or not having been clinical in the ground clearing process beforehand. It will however, grow between concrete slabs and can ‘penetrate’ the cement that bonds bricks / stone in its quest for light and water by exploiting the ‘weakest’ point. A very subtle difference in terminology yet poles apart in reality. You may have heard that the plant can ‘destabilise foundations’ or ‘grow through solid concrete’? These statements are very misleading to say the least and regrettably, sometimes used by some less reputable contractors to cause anxiety to the property owner, with the ultimate objective being financial gain.

“It will grow through concrete” and “until it is gone, you won’t be able to sell the house” –That claim, was made to us back in 2010. Not surprisingly is a complete fallacy.

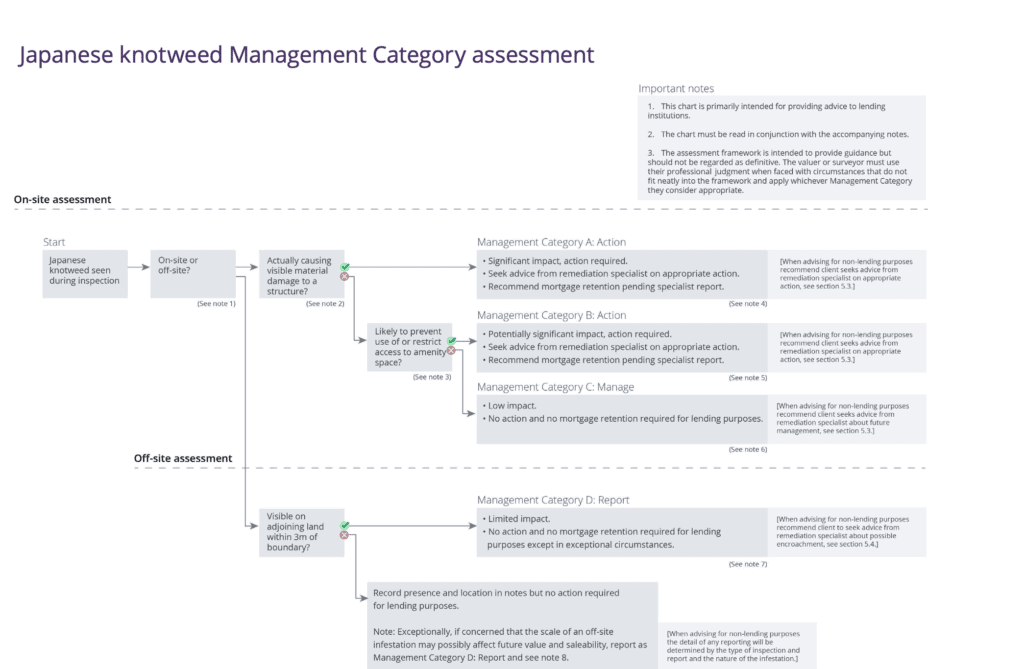

Cautionary Note – As of February 2022, the below RICS chart which was used for a number of years to ‘categorise’ Japanese Knotweed, is now outdated and has since been replaced by a new format. However, we have left the chart on our website as it remains to be seen how & when the UK mortgage lenders will adapt to the new guidance (see below). In our experience, even though the new guidance has been proposed for a considerable time and was ratified by all the pivotal stakeholders (including the council for mortgage lenders), the UK mortgage lenders are known to be quite stringent when assessing perceived ‘risk’. It’s an irrefutable fact that the lenders follow their own protocols when considering a mortgage application. The most trivial of matters may be an issue for one lender, yet may not be for another.

As a consequence, we predict that a gradual change of protocol will become apparent, as opposed to an imminent adaption of what has been used for the last 10 years or so. Therefore, whilst we as a contractor will follow the new guidance note, it may well be that some lenders are still working under the ‘old’ RICS chart.

Ultimately, unless the mortgage lender is appeased, they are unlikely to lend you the money!

| Category | Description |

| 4 | Japanese Knotweed is within 7 metres of a habitable space, conservatory and/or garage, either within the boundaries of this property or in a neighbouring property or space; and/or Japanese Knotweed is causing serious damage to outbuildings, associated structures, drains, paths, boundary walls or fences and so on. |

| 3 | Although Japanese Knotweed is present within the boundaries of the property, it is more than 7 metres from a habitable space, conservatory and/or garage. If there is damage to outbuildings, associated structures, paths and boundary walls and fences, it is minor. |

| 2 | Japanese Knotweed was not seen within the boundaries of this property, but it was seen on a neighbouring property or land. Here, it was within 7 metres of the boundary, but more than 7 metres away from habitable space, conservatory and/or garage of the subject property. |

| 1 | Japanese Knotweed was not seen on this property, but it can be seen on a neighbouring property or land where it was more than 7 metres away from the boundary. |

OLD RICS chart – superseded February 2022

GET STARTED TODAY

Whilst the previous ‘risk categories’ detailed above) were used as the framework for the mortgage lenders to decide on whether to approve or decline a mortgage application, it is fair to say that the structure was outdated and not fit for purpose. The so-called ‘7m rule’ focused more on what has been demonstrated to be an overstated risk of Japanese knotweed to buildings, rather than its potential impact on amenity (we now know that the roots seldom spread more than 3m laterally).

New Assessment Process

The new assessment process enables the valuer or surveyor to carry out a structured assessment, that leads to an objective categorisation. It is a more a definitive guide as to the full extent of an infestation and allows the ‘real impact’ of any given infestation, relative to its location and the specifics of the affected property to be established.

Although there are similarities to the assessment process, instead of the previous risk categories, the new guidance is focused on ‘Management Actions and will focus on matters such as loss of amenity space and actual damage to structures. The previous 7m rule of Japanese Knotweed being visible beyond a property boundary, has been replaced with 3m. The main objective of the Management Category assessment process is to provide consistency across the residential property market so that all stakeholders can understand the significance (or lack of) of Japanese Knotweed at or near any given property.

Before & After

The ‘new’ categories are detailed below:

Management Category A – Action required.

Management Category B – Potential significant impact. Action required.

Management Category C – Low Impact

Management Category D – Limited Impact.

Client note – We anticipate that it’s highly likely any property deemed to be management category A or B, will almost certainly trigger the requirement for a Japanese Knotweed Management Plan (JKMP), supplemented by a 5 or 10-year Insurance Backed Guarantee (IBG) (again, that’s not conclusive, it’s merely what we foresee will happen sooner or later). As we advance with time, we also predict that an infestation fitting the criteria of a management category C & D is far less likely to be an issue for the lender.